Introduction

A cashflow ladder is simply about having the right money available at the right time to spend. But it is also about protecting the money you’re due to spend in the short term from unhelpful market movements.

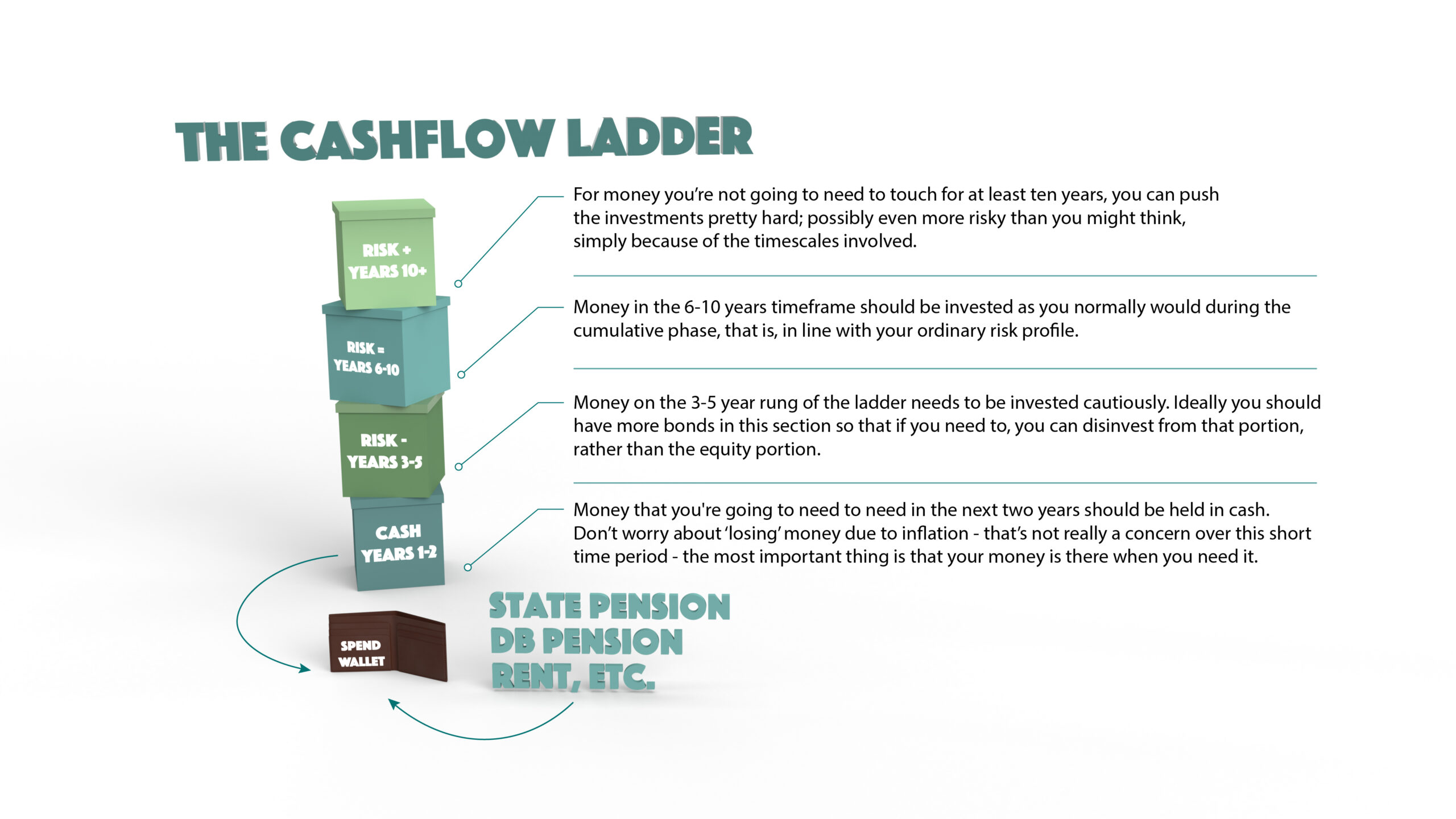

I’ve produced an outline diagram of what the cashflow ladder looks like and you can view it here. The basic premise is that you ladder your portfolio, for which, read pension funds and ISAs – for most of us at least – based on the timescale in which you’re going to access that money.

Knowing what our cashflow needs are likely to be for the next five years means we can keep this money in cash or very low-volatility investments. Money which we know we’re not going to need for, say, six years or more can be invested for growth, knowing that we can let any fluctuations ride out for a while yet.

The rationale is that if you keep two years’ spending needs in cash, then you shouldn’t need to access the invested part of your portfolio while it is sitting on a loss because almost all market dips return to some kind of normality within two years, and particularly if you have a well-diversified portfolio across different geographies.

This doesn’t always work; it took some of the major stock markets nearly six years to recover their value, even with income reinvested, after the great financial crisis. This was a singular event, a definite outlier, but that’s not to say it can’t or won’t happen again.

The Cash Flow Ladder

So to do this exercise, picture a ladder with four levels, or a set of four boxes placed one on top of the other. Draw it out if you like, or use my example. At the bottom is the money you’re going to use in years 1 and 2 – this should be kept in cash. No arguments; there should be zero risk attached to this money.

You’re going to spend it in two years; it should be risk-free and for that it needs to be cash in the bank or building society, premium bonds or whatever. Don’t worry about interest rate – this is not about earning money, it’s about that money being there risk-free.

The second box is for years 3-5 – this should be invested at a lower-risk level than you might ordinarily be comfortable with. It might be that you’ll need to spend some of this while it’s still invested. If we get another financial crisis, you might have to dip into it, so it should have a larger-than-you-might think element of bonds in it. Low-volatility, investment-grade government bonds ideally.

If you’re a Balanced investor by nature, and we equate that to a 50:50 equity:bond portfolio, then you might want to dial your equity content in this box down to, say, 30%, with 70% in bonds. The point is that you should have a good bond portion you can access in a pinch, because it should be less vulnerable to market movements. That’s a huge generalisation, I know!

Ladder rung or box number three is your years 6-10 box. So you know you’re not going to access this money for at least five years. This means you can afford to invest just as you would have done when accumulating, in other words, in line with your standard attitude to risk.

Finally, the top rung is for money you know you’re not going to need for at least 10 years. This means you can really push this money hard to get the growth you’re going to need to beat inflation over the longer term.

Essentially that’s it, except of course that it isn’t. What about the split between pension and ISA, for example? Well, it’s easy to overthink this, but if I were planning for you, I’d be telling you not to try to predict where you’re going to need to take money from for every year throughout retirement – there are just too many variables over such a long period of time.

Instead, look ahead just five years. If you see that you’re not likely to have any earned income in that time, you’re going to want to consider using pension withdrawal to take up your personal allowance perhaps, and so you’ll need to make sure some of the money in your pension is positioned correctly on the ladder to draw down at the right time.

That might mean some money sitting in cash or near-cash for longer than might feel sensible. Also, everyone’s risk capacity is different. Everyone’s capacity for weathering market dips is different. The ladder is a framework to help you not have to worry about that too much, but still, our behaviour is a factor.

{kind=link}

Leave a Reply